Ghanaian actor Kofi Adu popularly known as Agya Koo has recounted a very dark moment in his life when he almost got beaten and killed after visiting a lady.

The actor who was speaking during one of his podcast revealed that during the early part of his life when he hadn’t entered kumawood and was a shoemaker in town he became friends with a bar owner who he mostly visited.

The Minority Leader of Parliament, Alexander Kwamina Afenyo-Markin, has strongly criticised the Economic and Organised Crime Office (EOCO) over the continued detention of the Ashanti Regional Chairman of the New Patriotic Party (NPP), Bernard Antwi Boasiako, and the bail conditions set for his release from custody.

Expressing strong displeasure with the state institution, Afenyo-Markin described EOCO’s actions against the politician, also known as Chairman Wontumi, as biased, suggesting that the arrest may have been driven by retaliation or vengeance.

He condemned the events, stating that such actions must not be condoned.

“It is clear that with what is happening, the EOCO is being capricious, biased and we must not entertain it,” he said while addressing the floor of Parliament on Thursday, May 29, 2025.

Bernard Antwi-Boasiako, popularly known as Chairman Wontumi, was arrested and detained by EOCO after reporting to the Criminal Investigations Department (CID) of the Ghana Police Service on Tuesday, May 27, 2025.

On Monday, May 26, 2025, he had reported to the CID, where he was formally charged with engaging in illegal mining activities.

According to a police statement signed by Superintendent Joseph Benefo Darkwah, Head of the Public Affairs Unit at the CID, the NPP regional chairman was cautioned over alleged involvement in unauthorised mining operations, pollution of water bodies, and entering a forest reserve without permission.

The police confirmed that Chairman Wontumi cooperated fully with investigators, provided his statement, and was subsequently granted bail with two sureties.

His detention by EOCO comes in the wake of a failed attempt by security operatives to arrest him on Friday, May 23, 2025.

MAG/MA

Also, watch the latest news in Twi on GhanaWeb TV below:

Minority MPs in Parliament have staged a walkout in protest of the continued detention of New Patriotic Party (NPP) Ashanti Regional Chairman, Bernard Antwi Boasiako, popularly known as Chairman Wontumi.

Chairman Wontumi was arrested by the Economic and Organised Crime Office (EOCO) on Tuesday, May 27, after he reported to the Criminal Investigation Department (CID) for questioning. He was subsequently held at the EOCO head office in Accra.

His lawyer, Andy Appiah Kubi, confirmed to Graphic Online that his client is being investigated on allegations of causing financial loss to the state.

He was subsequently granted bail of GH¢50 million with two sureties, both to be justified.

Chairman Wontumi, however, spent the night behind bars at the EOCO headquarters in Accra after failing to meet the full bail conditions.

Speaking on the floor of Parliament on Thursday, May 29, Mr Afenyo-Markin declared that the Minority would boycott all parliamentary proceedings until the EOCO reviews and varies the bail conditions of Chairman Wontumi and releases him from custody.

“The NPP side, however, our numbers, we will protest by absenting ourselves from the proceedings of this House,” the Minority Leader said.

He called on his colleagues on the Majority side to stand in solidarity.

Prior to the walkout, the Minority MPs rose to their feet, chanting a line from Ghana’s national anthem — “and help us to resist oppressors’ rule with all our will and might forevermore.”

They repeated the same anthem’s line in a symbolic act of defiance while they walked out.

The MPs after walking out of the chamber announced that they were trekking to the offices of EOCO which is about 30 minutes away from the premises of Parliament.

DISCLAIMER: The Views, Comments, Opinions, Contributions and Statements made by Readers and Contributors on this platform do not necessarily represent the views or policy of Multimedia Group Limited.

DISCLAIMER: The Views, Comments, Opinions, Contributions and Statements made by Readers and Contributors on this platform do not necessarily represent the views or policy of Multimedia Group Limited.

The Member of Parliament for Ejisu constituency, Kwabena Boateng has donated 200 dual desks to the Onwe Senior High School.

This follows Channel One News’ report highlighting significant challenges confronting Onwe SHS, including inadequate furniture.

The school faces numerous challenges, such as inadequate classrooms, a science lab, an ICT lab, and projectors.

The Member of Parliament for Ejisu has vowed to address the issues and other educational challenges in the constituency.

“I have been told they have other needs, which I have taken note of. I’m told there’s a science lab that has to be completed and lab materials that will aid science education. I will look for the next money, I’m interested particularly in Onwe SHS as much as other schools within my jurisdiction,’ he pledged.

Speaking to Citi News, some students said the donation of chairs will ease the pressure of sitting on the floor and standing during learning hours and examinations.

“We thank the MP for the gesture, our lack of interest in going to school has eased. Now we can go to school knowing that we will have chairs to sit on to study. It was a problem for us because most of us don’t see it to be a good place for us because we are struggling too much,” One of the students said.

Another student said, “Most of us were leaving school for the house. Now we wish to be in class every day.”

They called on the government to intervene and address other issues confronting the school.

“The government should come to our aid and develop the school; individuals should also come to our aid by building a science lab, an ICT lab, boarding houses, etc.”

“Students used to sit on the floor to write exams. We’ve been running shifts during exam days, which has been a challenge for us.

Another student stated, “We’re many, and when we have meetings, teachers sit on tables and students sit on the floor. We’re very happy, the chairs will improve our dedication. We’re calling on the government to come to our aid.”

The Assistant Head in charge of Academics, Monica Addai-Appiah urged the government to come to their aid.

“We’re very grateful to Hon. MP, we’re all happy, the students, teachers, and I are all happy. We desperately need the chairs. Getting chairs has been our greatest challenge.

“We need a three-in-one printer machine, projectors for classrooms, a science lab, not completed, mathematical sets. We call on the government to complete the boarding house for us to ease the congestion in the classrooms,” she appealed.

Health Ministry: Nearly 100,000 trained health workers unemployed

…..

Explore the world of impactful news with CitiNewsroom on WhatsApp!

Click on the link to join the Citi Newsroom channel for curated, meaningful stories tailored just for YOU: https://whatsapp.com/channel/0029VaCYzPRAYlUPudDDe53x

No spam, just the stories that truly matter! #StayInformed #CitiNewsroom #CNRDigital

Entertainer and social media personality Charles Oputa, popularly known as Charly Boy, has berated the senator representing Abia North, Orji Kalu, over his outfit endorsing President Bola Ahmed Tinubu for a second term.

Naija News reports that Kalu attended Tuesday’s plenary at the senate wearing an outfit bearing the inscription ‘Tinubu for President 2027′.

At least ten individuals have been arrested for engaging in illegal mining activities near the Akyem-Abomosu STEM school in the Eastern Region.

The arrests were made during a special operation led by the Administrator of the Minerals Development Fund, Dr. Hannah Louisa Bissiw, in collaboration with the Atiwa West District Chief Executive, Amo Johnson Anom.

The joint operation—comprising Police personnel, Immigration officers, and the Atiwa West District Taskforce—set off from the district assembly premises, fully equipped for the task.

Upon arrival, the illegal miners attempted to flee but were chased into a nearby bush where ten Ghanaians and one Nigerien national were apprehended.

The arrested suspects include Opoku Kwabena, Ebenezer Obeng, Felix Opoku, Mporumbo Manda, Kwame Baguaputie, Moses Dakura, Yaba Kudebila, Luumah Hassan, Ishmael Annor, and Armah Abubakar from Niger.

The operation was triggered by the recent drowning of a 7-year-old boy in an abandoned mining pit at Akyem-Akrofufu. The boy had reportedly gone to play near the pit when he accidentally fell in and drowned.

Dr. Bissiw expressed her distress over the incident, noting that illegal miners have now moved from the forests into communities, posing increasing dangers to residents.

“Recently, a 7-year-old boy fell into a pit. These miners have moved into communities, mining close to schools and homes. They are driving students and teachers out of the STEM school by taking over its land,” she stated.

As part of efforts to hold polluters accountable, Dr. Bissiw announced that the Minerals Development Fund will soon implement the ‘polluter pays principle’ to compel environmental offenders to bear the cost of damage they cause.

“The Atiwa West DCE shares this principle—that when you destroy the environment, you must pay for it,” she added.

Several mining equipment, including an excavator, water pumping machines, a bulldozer, and motorcycles, were seized during the operation.

DCE Amo Johnson Anom issued a stern warning to community leaders, advising them not to lobby on behalf of those arrested.

“From tomorrow, some people will start coming to our offices to plead. I’m warning everyone: don’t come. If you do, we’ll hand you over to the police,” he warned.

According to him, all ten suspects will be arraigned before court once police investigations are complete.

Sidi Ould Tah has been elected as the new president-elect of the African Development Bank Group (AfDB) following a vote by the governors of the bank on Thursday, May, 29, 2025 during the bank’s 2025 Annual General Meetings held in Abidjan, Côte d’Ivoire.

Tah’s election makes him the 9th president of the bank and was officially announced by Niale Kaba, Minister of Planning and Development for Côte d’Ivoire, and Chairman of the Board of Governors of the Bank Group.

The winning candidates is required to obtain at least 50.01% of both the regional and non-regional votes.

Tah a Mauritanian economist brings over 35 years of experience in African and international development finance.

He served as President of the Arab Bank for Economic Development in Africa (BADEA) from 2015, where he spearheaded a major transformation, quadrupling the bank’s balance sheet and earning it a AAA credit rating.

He also served as Mauritanian’s Minister of Economic Affairs and Finance and has held influential sector reform, and resource mobilisation, notably overseeing the launch of BADEA’s $1 billion callable capital program to support African multilateral development banks.

The Board of Governors Steering Committee received and approved a total of five candidates by the closing date of 31 January 2025. The list of candidates was officially announced on 21 February 2025.

Sidi Ould Tah will assume office on 1 September 2025, for a five-year term, following the end of the second mandate of current President, Dr Akinwumi Adesina.

The other candidates in the election were:

Amadou Hott (Senegal)

Samuel Maimbo (Zambia)

Mahamat Abbas Tolli (Chad)

Bajabulile Swazi Tshabalala (South Africa)

Sidi Ould Tah elected ninth president of the African Development Bank Group.

● The Porcupine Warriors are desperate to augment their squad for next season.

● They are hoping to qualify for Africa and have identified their former glovesman as a key man to beef up their goalkeeping department.

Top Ghanaian goalkeeper, Razak Abalora is set to make a sensational return to his former club, Asante Kotoko after the ongoing campaign.

The 28-year-old shot-stopper, who left the Porcupine Warriors three years ago, currently plies his trade with AF Elbasani in Albania.

Following Abalora’s departure in 2022, he joined Moldovan side, Sheriff Tiraspol on a three-year contract. This made him the fourth Ghanaian player to join the club in the space of two years.

He later switched camp to sign a three-year deal with Albanian side, AF Elbasani last year.

Despite spending just one season in the Albanian league, the 28-year-old goalkeeper is expected to cut his stay short to rejoin his former side next season.

As confirmed, the GPL giants are reported to have held initial discussions with the goalkeeper with the future of Frederick Asare hanging on a thread.

Although the club has reportedly agreed terms with Asare for a contract renewal, uncertainty surrounds his future due to limited playing time this season.

Abalora ended the 2024/25 season as one of the best goalkeepers in the Albanian league, helping his side to finish 5th with 50 points.

He appeared in 27 games for AF Elbasani while keeping 9 clean sheets.

Senior Fellow at the Institute of Economic Affairs, (IEA), Dr. Vladimir Antwi-Danso, has called on the government to focus on export driven by local production in order to sustain the current appreciation of the cedi.

Dr. Antwi Danso who made the call at the IEA public forum on the theme, “Trump Tariffs: Implications for Africa and Ghana,” said though the cedi has recorded positive gains it may not stabilise permanently without adequate reforms.

“We must try and be an export economy, and that is the only way you stabilize your currency. That is the only way you make the other currency lower or stronger, the appreciation of the cedi may soon reverse.

“What we are doing is that we are not stabilising permanently, we will relapse. By December, I believe we will relapse. And I’m saying this from a technical point of view, not as a political comment. What I’m trying to say is that it’s not yet ‘hooray’ for a cedi kind of appreciation,” he stated.

He also asked President Mahama to take measures to prevent Ghana from returning to the International Monetary Fund (IMF) at the end of the current programme after the end of the current programme.

“The president has given indication that it is a legacy term. If it’s a legacy term then I suspect he must put things right so we don’t go back. It is a routine ritual, this is the 17th and there is no indication that this is going to be the end. It is because of the spending spree especially during election years,” he said.

“During election years, we throw everything to the dogs and spend the way we spend and the spending is not such that it is bringing back the money we are spending. It is just for consumption. We borrow for consumption,” he added.

The discussions emphasised the urgent need for sustainable economic strategies that reduce reliance on imports and build resilience through value-added exports and industrialization.

The forum also brought together economists, policymakers, and members of the diplomatic and business communities to discuss the impact of global trade especially on tariffs especially at the time when the cedi is fast appreciating against other major currencies.

Deputy Minority Leader, Hon. Patricia Appiagyei, has announced that the Minister for Foreign Affairs, Samuel Okudzeto Ablakwa, will be summoned to explain the brief closure of Ghana’s embassy in Washington, DC in Parliament.

She describes the action taken by the foreign minister as reckless and diplomatically costly, considering that he failed to consult parliament.

During a media briefing by both caucuses in Parliament on issues programmed to be considered on the floor of the House at the Second Meeting of

The Ghanaian economy is not only stabilizing, but it is also opening up for quality investment, Bank of Ghana Governor Dr Johnson Pandit Asiama has said.

He says that as confidence returns to our macroeconomic environment, we are seeing a clear window to reposition Ghana as a preferred investment destination in West Africa.

Explaining why this is so, he said, first, there is policy stability.

Ghana’s economic strategy is anchored on monetary discipline, fiscal prudence, and structural reform.

“This is not just about meeting IMF programme conditions; it’s about restoring credibility, rebuilding buffers, and laying the foundation for resilient, inclusive growth,” he said.

The consistency of our recent policy moves from inflation targeting to FX market reform reflects this deeper shift, he added.

Second, he stated, the real sector fundamentals are strong.

“We recorded 5.7% GDP growth in 2024, and we are on track for 4.0% growth in 2025, even in a globally uncertain environment. Recovery in private sector credit, improving consumer demand, and expanding export earnings — particularly from gold, cocoa, and services — all point to a more diversified and opportunity-rich economic base,” he said ruing a Private Investor Roundtable at the African Development Bank (AfDB) Annual Meetings on Wednesday, May 28.

Third, he said, Ghana’s financial sector is stable and improving. Capital Adequacy Ratios have strengthened, reaching 15.8% in April 2025 even without regulatory relief.

“Liquidity levels are improving, and though non-performing loans remain elevated (23.6%), the effective provisioning of losses and BoG’s close supervisory role are helping restore resilience. We are also investing in digital finance, payments interoperability, and fintech innovation — not only to boost financial inclusion but to enhance systemic efficiency,” Dr Asiama said.

Dr Asiama also stated that beyond the numbers, what truly makes Ghana stand out is its readiness to partner with private capital.

“We are developing opportunities across several key sectors: Green energy and sustainable infrastructure aligned with Ghana’s climate transition goals; Digital innovation and fintech, building on the success of platforms showcased at the recent 3i Africa Summit; Light manufacturing, logistics, and agribusiness, with potential linkages to regional value chains under the AfCFTA framework,” he said.

He added “Investors are not just looking for returns — they are looking for stability, governance, and strategic alignment. Ghana offers all three — and we are building the institutions to keep it that way.”

Renowned playwright and motivational speaker Uncle Ebo Whyte has advised individuals to avoid being forced into marriage to conform to societal norms.

In a video posted to his Instagram handle, Uncle Ebo, who has been married for 42 years, challenged long-held societal expectations about marriage, urging young people not to feel pressured into tying the knot.

When asked about the purpose of marriage, he said, “There was a time when everybody needed to marry. That time has changed.

“There was a time when there was a purpose of marriage. That time has changed. There was a time when we needed to marry. That time has changed. It’s not now,” he said.

Citing the Apostle Paul’s teachings, he said, “He who marries does well. He who does not marry does even better.”

Uncle Ebo also addressed arguments surrounding procreation and companionship, noting that family planning has shifted the role marriage once played in society.

“Because now we are saying there are too many people. Let’s control the population. Then there’s the issue of companionship. I’ve been married for 42 years. Companionship…” he said.

The celebrated writer also cautioned against romanticising marriage, describing it as a relationship that requires “hard work, patience, humility, and respect,” not just love.

“Marriage is not given to everybody. Not everybody needs to marry. Not everybody will marry. Marriage is not a magic wand. It may not deliver half of what you expect. So if you do choose to marry, do so because you’ve found someone with whom you genuinely want to build a life, not because society says you must,” he added.

Uncle Ebo concluded by reminding his audience that one’s value is not determined by marital status and that people can live fufilled lives without marrying.

“You are complete with or without marriage. Some of the most fulfilled people I know never married, and that’s perfectly okay,” he said.

Kwesi Pratt Jr, the Managing Editor of the Insight Newspaper

The Managing Editor of the Insight Newspaper, Kwesi Pratt Jr, has weighed in on the crackdown on Ghana’s embassy in Washington DC in the USA by the Ministry of Foreign Affairs.

While applauding the move intended to sanitise the diplomatic mission installation, he cautioned that the ministry could have been more discreet in their approach.

Speaking on Metro TV on Wednesday, May 28, 2025, Pratt underscored the importance of safeguarding the integrity of the Ghana’s High Commissions and embassies around the world.

He cited a scenario where a media house opened phone lines to solicit views from Ghanaians in the diaspora on the matter.

He described the process as being not just alarming but detrimental to Ghana’s missions.

“The things they were saying were horrible. I want to believe that the Ghanaians who were calling were sincere and they spoke the truth. But what is the effect of that on the ability of our missions to represent the country in other parts of the world?

“If we create an impression that our High Commission and our embassies are a den of crooks and a group of highway men and women, we do irreparable damage to the reputation their capacity to represent us properly,” he said.

He noted that the brouhaha surrounding the scandal at the Washington DC does not only taint the image of our missions in foreign jurisdictions but weaken their influence to represent the country to the global community.

“First of all, one has to make the point that His Excellency Samuel Okudzeto Ablakwa has earned a huge reputation, as an anti-corruption campaigner and there’s no doubt at all about that.

“Having said that I think the point has to be made that many diplomatic missions have had problems in many countries, not just in Ghana. A couple of years ago. I think about two years ago, South Africa suspended the issuance of visas from their High Commission here. No noise was made about it. We (those of us who travel to South Africa a lot) just noticed that the process had become slow and it went by unexplained.

“It took a long time for us to realise that there was a problem with the issuance of visas from the South African High Commission here. They kept it under wraps. Not just that I have known at least, on one occasion, that a British diplomat had been recalled from Ghana,” he said.

He explained that several missions in Ghana and elsewhere have had problems but it was dealt with quietly.

“There must be a reason for that. It seems to me that the reason is that given the role played by High Commissioner and its importance, they must be viewed with a certain decorous frame,” he said.

He stressed that the integrity of Ghanaian embassies have been bruised by this development, a situation he finds worrying.

Background

A local staff at the Ghanaian embassy in Washington DC in the USA, identified as Fred Kwarteng, was dismissed by the Minister of Foreign Affairs, Samuel Okudzeto Ablakwa, for engaging in alleged corrupt practices.

In a statement on May 26, 2025, by the Minister of Foreign Affairs, Samuel Okudzeto Ablakwa, he announced that Fred Kwarteng, a local staff recruited in 2017 to work at the embassy had reportedly illegally diverted visa and passport applicants into his privately owned company called Ghana Travel Consultants.

According to Ablakwa, Kwarteng upon interrogation admitted to using his private company to charge extra fees for multiple services without the knowledge of the Foreign Affairs Ministry and additionally kept the entire revenue generated in his private account.

“Mr Kwarteng was a local staff recruited on August 11, 2017 to work in the embassy’s IT department. According to findings and his own admission, he created an unauthorised link on the embassy’s website which diverted visa and passport applicants to his company, Ghana Travel Consultants (GTC) where he charged extra for multiple services on the blind side of the ministry and kept the entire proceeds in his private account,” the minister indicated on Monday, May 26, 2025.

The fees charged by Kwarteng were not approved by either the Ministry of Foreign Affairs or Parliament, thereby constituting a violation of the Fees and Charges Act.

“His illegal extra charges which were not approved by the ministry and parliament as required under the Fees and Charges Act ranges from US$29.75 to US$60 per applicant. The Investigations reveal that he and his collaborators operated this illegal scheme for at least 5 years,” the statement added.

Ablakwa added that, in addition to the individual’s dismissal, the matter has been referred to the Attorney General for further punitive action.

VPO/MA

Meanwhile, catch up on the concluding part of the story of Fort William, where children were sold in exchange for kitchenware, others, below:

Africa Policy Lens (APL), a Policy Research and Analysis Organisation has commended Ghana’s recent macroeconomic progress but warned that the appreciation of the cedi could be short-lived if not supported by deeper structural reforms.

According to APL, while the cedi has appreciated significantly in the first half of 2025, this has largely been driven by temporary measures.

It mentioned heavy forex market interventions by the Bank of Ghana (nearly $1 billion between January and May 2025) and tough fiscal decisions such as freezing government spending and suspending payment of arrears as factors that have significantly contributed to these gains.

“These gains, while encouraging, are built on temporary pillars that require deeper reforms to become sustainable,” APL noted.

APL points out that Ghana has seen similar periods of stability before, particularly between 2017 and 2019 during the IMF Extended Credit Facility program.

During that time, the cedi was relatively stable due to improved fundamentals, disciplined fiscal policy, and external conditions such as rising oil production and commodity prices.

APL suggests that today’s policymakers can learn from that period by focusing on long-term reforms instead of relying on interventions.

“There are lessons from the past—particularly the 2017–2019 period—that show sustainable stability must be anchored in strong fundamentals, not ad hoc measures,” the organisation stated.

In a press release issued on Tuesday, May 27, 2025, it highlights potential risks if current strategies continue without adjustment while warning that the over-reliance on gold-backed interventions and deferred obligations could backfire, especially if commodity prices fall or external financing becomes more difficult.

“Over-reliance on short-term tools such as gold-backed forex support and deferred government obligations could leave the economy vulnerable to external shocks,” APL warned.

It indicated that analysts such as S&P Global Ratings and Fitch Solutions have already warned that the cedi could face renewed depreciation in the second half of 2025 if structural imbalances resurface.

“Global credit watchers are already flagging risks, and Ghana must act swiftly to insulate itself from renewed pressures,” APL emphasised.

APL calls for stronger policy action, including the completion of debt restructuring, diversification of export revenue sources, and improved fiscal management. It also emphasises the importance of transparent communication from government institutions to maintain investor confidence.

“To maintain the current momentum, reforms must be bold, and communication must be clear to avoid spooking markets,” the group stated.

In conclusion, APL states that while Ghana’s currency has shown impressive recovery, “the challenge now is to ensure these gains are not only preserved but built upon,” reiterating that “without long-term reforms, the current stability may not hold.”

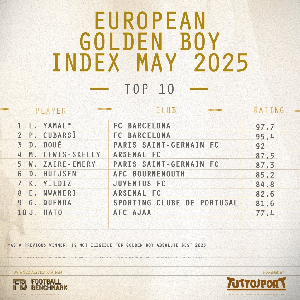

Lamine Yamal (L), Arda Guler (M) and Desire Doue (R) have been nominated for the Golden Boy Award

The 100-player shortlist for the prestigious 2025 Golden Boy award has been released.

While familiar names like Lamine Yamal, Arda Güler, and Desiré Doué dominate the headlines, it’s Barcelona centre-back Pau Cubarsí who is emerging as the frontrunner for this year’s title.

Published by Tuttosport, the organisers of the award, the latest Golden Boy Index ranks Cubarsí second overall with a strong chance of claiming the honour.

He is the highest-placed eligible player after Lamine Yamal, who tops the current index with a rating of 97.7 but cannot win again after lifting the trophy in 2024.

Also high in the latest rankings are Desiré Doué of Paris Saint-Germain (3rd), Arda Güler of Real Madrid, and Kenan Yildiz of Juventus (7th), the latter being the only Serie A-based player in the current top 10.

France lead the way with the most nominees (17) on the 100-man list, underlining the country’s continued strength in youth development. Belgium (10), Spain (8), and England (8) follow closely behind.

Italy have just two players on the list, Pietro Comuzzo (18th) and Giovanni Leoni (99th), although five players currently plying their trade in Serie A made the cut, including Alex Jimenez (69th), Kenan Yildiz (7th), and Diao del Como (28th).

One standout name in the top 10 is Dean Huijsen, ranked 6th, who recently completed a move from Bournemouth to Real Madrid ahead of the 2025/26 season.

Another is Jan-Carlo Simic, formerly of AC Milan and now at Anderlecht, ranked 24th.

The award, launched in 2003, is presented annually to the best Under-21 footballer in Europe based on performances across domestic and international competitions.

Check out the top 10 nominees below:

FKA/MA

Also, watch the latest news in Twi on GhanaWeb TV below:

President John Dramani Mahama has commenced a three-region “Thank You” tour, beginning Thursday, May 29, in the Bono East Region.

The tour is part of his nationwide appreciation campaign to express his heartfelt gratitude to the people of Ghana for the overwhelming support and confidence they showed in him during the December 2024 general elections.

The President is expected to address a grand durbar of chiefs, opinion leaders, and residents in Bono East, where he will personally thank them for their massive turnout and the resounding endorsement they gave him and the National Democratic Congress (NDC) at the polls.

The durbar will serve as an important platform for President Mahama to reaffirm his commitment to inclusive leadership and participatory governance.

In addition to expressing gratitude, President Mahama will also take the opportunity to outline his administration’s development agenda for the region.

He is expected to unveil a number of priority projects tailored to meet the specific needs of the people, with a focus on job creation, youth empowerment, education, healthcare, and infrastructure development.

The Minister of Sports and Recreation, Kofi Adams, has called for climate leadership in the world of sports, unveiling a series of green initiatives at the Global Sports and Sustainability Forum 2025 held in Cape Town, South Africa.

Addressing an international audience of policymakers, sports executives, and climate advocates, the Minister urged countries to reimagine sports infrastructure as a catalyst for environmental resilience and community development.

Hosted by SPORTS20 under the theme ‘Another World Is Possible,’ the event featured voices from around the world exploring how sport can confront global crises like climate change and biodiversity loss.

In his opening remarks, the Minister emphasised that sport is both a victim and a contributor to climate change, citing the examples of flooded pitches, rising temperatures, and unpredictable weather that disrupt competitions and training schedules.

Kofi Adams also hinted that the John Mahama-led administration will soon launch a new National Recreation Agency, tasked with leading a climate-conscious wellness movement.

Among its flagship programmes will be National Recreation Day and National Aerobics Day, both designed to engage citizens in tree planting, clean-up campaigns, and climate-friendly sporting events.

The Minister also addressed the environmental devastation caused by illegal small-scale mining, or galamsey and said Ghana will develop community sports academies and green parks on degraded lands in collaboration with mining companies, offering young people alternative livelihoods through sports.

The Minister praised SUCCA Africa, GHALCA, and SPORTS20 for their role in advancing the Green Futball Initiative, which has brought climate issues into the heart of Ghana’s sports culture.

GHALCA President John Ansah for his part said African football has a unique opportunity to lead by example in sustainability and commitment to green practices will not only protect the environment but also inspire future generations to embrace eco-friendly sportsmanship.

President John Dramani Mahama has indicated that his government does not aim to achieve an exchange rate where the value of the dollar can be equated to the cedi.

Speaking at a high-level presidential session at the 60th Annual Meeting of the African Development Bank (AfDB) and the 51st Annual Meeting of the African Development Fund (ADF) in Abidjan, the Ghanaians president shared the adverse effect such a rate could have on the economy.

The president explained that the Ghanaian economy would risk losing a significant

Naomi Oyoe Ohene Oti received a heroic welcome at KIA after receiving the global nursing award

Oncology Nurse Specialist at the Korle Bu Teaching Hospital, Naomi Oyoe Ohene Oti, has returned to Ghana after winning the 2025 Aster Guardians Global Nursing Award of $250,000.

A viral video capturing her return to Ghana shows an emotional and heartwarming scene as colleagues and family gathered to cheer and welcome her at the Kotoka International Airport on Thursday May 29, 2025.

The crowd erupted in song and dance, waving Ghanaian flags.

Naomi Oyoe, who serves as Head of Nursing at the National Radiotherapy, Oncology and Nuclear Medicine Centre at Korle Bu, received the award during a grand ceremony held in Dubai on May 26,2025.

She was recognised for her transformative work in cancer care, which has made a measurable impact not only in Ghana but across the African continent.

Chosen from among 100,000 nominees representing 199 countries, she stood out as one of ten finalists honoured at the event, each of whom was presented with a plaque of participation.

The Aster Guardians Global Nursing Award is designed to spotlight extraordinary nurses who demonstrate innovation, compassion, and leadership in healthcare delivery.

In her acceptance speech, she expressed deep gratitude and a renewed sense of purpose.

“My passion for oncology nursing was born out of a desire to bridge this gap and deliver compassionate, high-quality care to those who need it most. This award affirms that dream and empowers me to do even more. It is more than recognition. It is a catalyst for lasting change. I am committed to using it to amplify the voice of African nurses, expand access to cancer care, and build a legacy of leadership and excellence in oncology nursing across our continent. This award, as said, is not mine alone”, she noted.

Watch the video below:

WATCH: How Naomi Oyoe Ohene Oti, Ghana’s oncology nurse and winner of the 2025 Aster Guardians Global Nursing Award, was welcomed home today!

Honoured with a $250,000 prize for excellence in cancer care, Naomi received a hero’s welcome at KIA. Channel One News’ Manuel Ayamah… pic.twitter.com/GDhgskV1e8

The National Road Safety Authority (NRSA) has issued a firm warning to Metropolitan, Municipal, and District Assemblies (MMDAs) within the Greater Accra Region, threatening legal action against those who fail to remove unauthorized billboards from road medians by Monday, June 2, 2025.

This follows a failed engagement with the assemblies, as many did not attend a scheduled meeting with the Authority to discuss a compliance roadmap.

Speaking to the media, NRSA Director-General Abraham Amaliba expressed disappointment at what he described as a defiant posture by the assembly members.

“We invited all of them through the Local Government Ministry. They misunderstood and assumed the invitation was extended to all assemblies nationwide, which is why some came from outside Accra,” he said.

“Those within Accra, who were required to attend, failed to show up. We are treating their absence as deliberate noncompliance, and we will proceed to sue the assemblies that have ignored our directive.”

According to Amaliba, the NRSA had initially given a 21-day deadline for the removal of the billboards and had intended to use the meeting to offer an extension. However, the absence of the relevant assemblies has left the Authority with no choice but to pursue legal action.

“This means they are not interested in complying. So, what we are going to do is meet them in court,” he added.

The NRSA insists the move is necessary to protect public safety, which it says is being jeopardized by the presence of unauthorised structures along roadways.

Recent cedi gains may be temporary without deeper reforms – APL

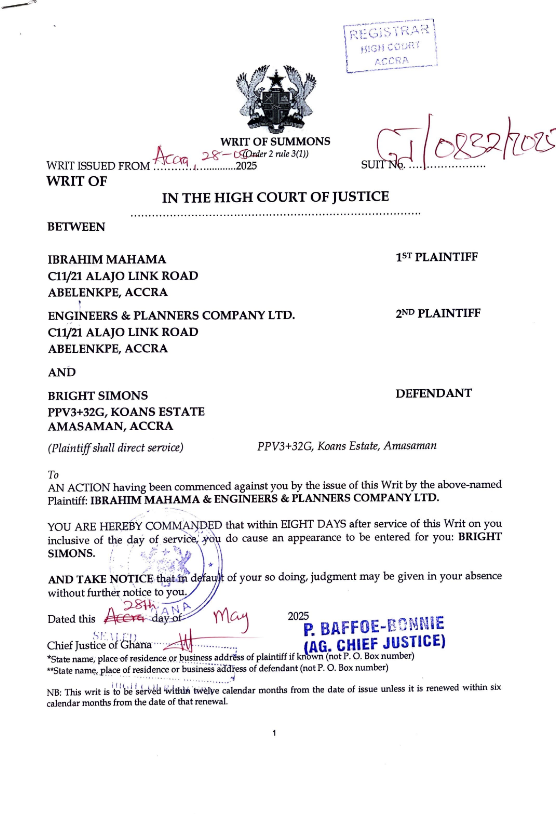

Businessman Ibrahim Mahama has filed a defamation lawsuit against Bright Simons, Vice President of IMANI Africa, over what he describes as a series of “false and malicious” publications that have damaged both his personal reputation and that of his company, Engineers and Planners (E&P).

According to court documents filed at an Accra High Court on May 28, Mahama and E&P allege that Simons made defamatory claims in an article titled “Ghana Provides a Lesson in How Not to Nationalise a Gold Mine” published on April 19, 2025, on his personal website, brightsimons.com.

On the same day, Simons shared the article via his official X (formerly Twitter) handle, @BBSimons, where it quickly gained traction. By May 8, the post had amassed more than 93,000 views, 250 reactions, 98 reposts, 26 comments, and 109 bookmarks.

The plaintiffs argue that this engagement contributed significantly to the wide dissemination of the alleged defamatory content.

The article reportedly accused E&P of financial distress due to halted operations at the Damang gold mine and suggested that the company’s creditors were “up in arms.” It also insinuated that Mahama, the brother of President John Mahama, was benefiting improperly from political connections, and that E&P was being unduly favored in government mining policies.

In their suit, the plaintiffs reject these claims outright, describing them as “entirely false and wholly without factual basis.”

They argue the article portrays E&P as financially unstable and undermines the company’s credibility with existing and potential business partners.

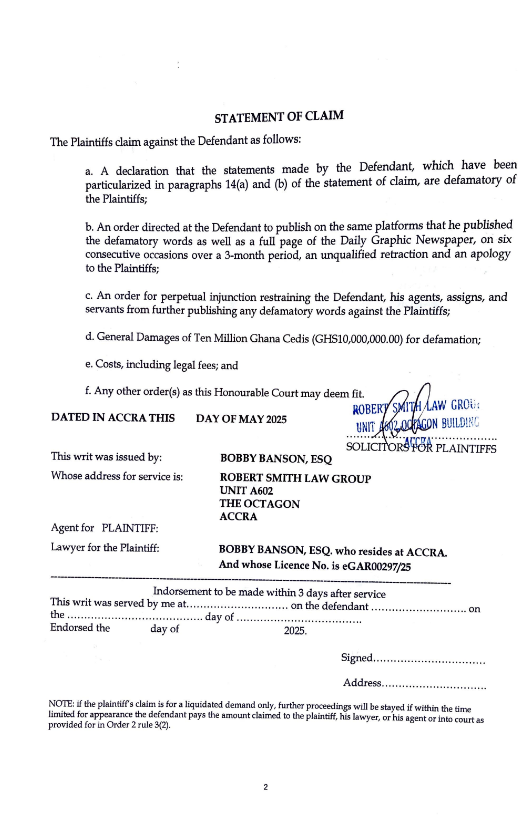

The plaintiffs are seeking the following reliefs:

A declaration that the statements made by Bright Simons are defamatory;

A public retraction and apology published on the same digital platforms and as a full-page ad in the Daily Graphic for six consecutive editions over three months;

A perpetual injunction barring Simons from making further defamatory remarks;

General damages amounting to GHS10 million;

Legal costs and any additional relief the court may deem appropriate.

GHANAIAN international model and philanthropist, Victoria Michaels has raised fresh concerns about the lingering exploitation in Ghana’s modelling industry, despite efforts at reform.

While strides have been made to empower models, exploitation remains a persistent issue due to a lack of regulations, professionalism and guidance for emerging talents.

In an exclusive interview with Graphic Showbiz, on Monday, May 26, the European Union Goodwill Ambassador stressed that although the industry was intended to be a platform for empowerment, the reality for many young models was far from ideal.

To her, the absence of clear structures leaves aspiring models vulnerable to manipulation, as many enter the field without contracts or the know-how to navigate its complexities.

“It’s a mixed reality. There are spaces of empowerment, but exploitation still exists, often due to a lack of regulation and professionalism. Many young talents enter the industry without proper guidance or contracts. That’s why mentorship is key. I see it as part of my responsibility to raise awareness and create platforms that protect and prepare them,” she said.

When asked whether Ghana’s fashion industry was ready for the global stage or was still leaning heavily on Western templates, she acknowledged the creative progress but admitted that deeper institutional challenges remained. (Read EDITOR’S LENS: Stop party politics in creative space post-elections)

“Ghana’s fashion industry has made tremendous strides, and there’s undeniable creativity and cultural richness here. However, while we are ready in spirit and talent, we still face structural and institutional challenges that hold us back from full global competitiveness,” she noted.

According to her, the industry’s journey towards originality and authenticity is gradually taking shape, even though the pressure for international validation continues to cast a shadow.

“There is also a lingering influence of Western aesthetics, often due to the desire for international validation. But I believe we’re at a turning point where originality, heritage and storytelling are becoming central to how we define Ghanaian fashion. Like I always say, we are not where we want to be,” she said.

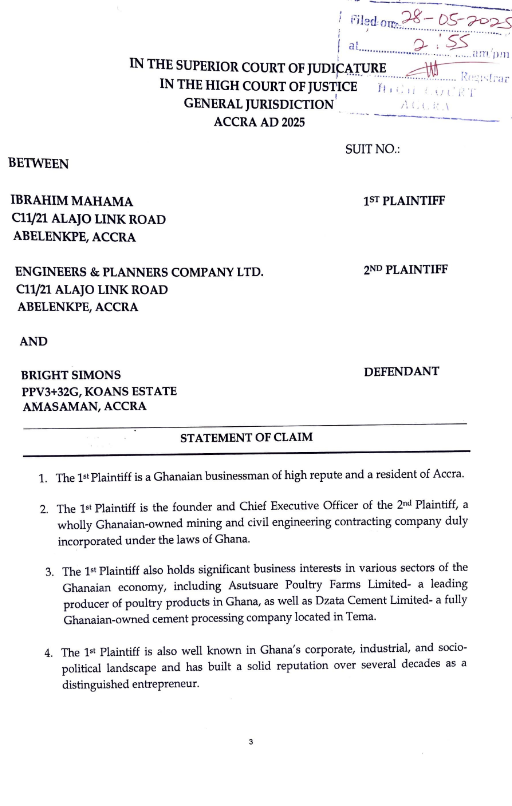

Ibrahim Mahama, who is a brother of President John Dramani Mahama, and his company, Engineers & Planners (E&P), have sued Bright Simons over what they describe as defamatory statements made in a recent article.

The article, titled “Ghana Provides a Lesson in How Not to Nationalise a Gold Mine”, was published on Simons’ personal website on Saturday, April 19, 2025.

The article discusses Ghana’s management of the Damang gold mine and includes claims that E&P, described as “a powerful operator owned by the brother of Ghana’s President”, suffered financially following a temporary shutdown of operations by Gold Fields.

Simons, a vice president of IMANI Africa, also raised concerns about E&P’s alleged influence on the Minerals Commission, suggesting potential conflicts of interest and political interference.

Ibrahim Mahama, in his application, sought damages of GH¢10 million, among other reliefs.

Below are the full claims in Ibrahim Mahama and his company:

a. A declaration that the statements made by the Defendant, which have been particularised in paragraphs 14(a) and (b) of the statement of claim, are defamatory of the Plaintiffs;

b. An order directed at the Defendant to publish, on the same platforms that he published the defamatory words, as well as a full page of the Daily Graphic newspaper, on six consecutive occasions over a 3-month period, an unqualified retraction and an apology to the Plaintiffs;

c. An order for a perpetual injunction restraining the Defendant, his agents, assigns, and servants from further publishing any defamatory words against the Plaintiffs;

d. General damages of Ten Million Ghana Cedis (GH¢10,000,000.00) for defamation;

e. Costs, including legal fees; and

f. Any other order(s) as this Honourable Court may deem fit.

Meanwhile, the High Court in Accra has ordered Bright Simons, a vice president of IMANI Africa, to file his defence in the defamation suit filed against him by business mogul Ibrahim Mahama.

Court documents sighted by GhanaWeb showed that the IMANI Africa vice president had been commanded to file his defence within 8 days of service.

The court said that if Bright Simons fails to enter his defence within the stipulated time, it will give its judgment on the matter without hearing from him.

“AN ACTION having been commenced against you by the issue of this Writ by the above-named Plaintiff: IBRAHIM MAHAMA & ENGINEERS & PLANNERS COMPANY LTD.

“YOU ARE HEREBY COMMANDED that within EIGHT DAYS after service of this Writ on you, inclusive of the day of service, you do cause an appearance to be entered for you: BRIGHT SIMONS.

“AND TAKE NOTICE that in default of your so doing, judgment may be given in your absence without further notice to you,” parts of the court document, which was issued by the Acting Chief Justice Paul Baffoe-Bonnie on May 28, 2025, read.

Following recent media reports about the alleged FBI arrest of Ghanaian business mogul Joseph Boateng, popularly known as Dada Joe, a spokesperson for has dismissed the claims as ‘fake’.

In an interview with GhanaWeb’s Joseph Henry Mensah on May 28, 2025, Fredrick Agyei stated that reports about the arrest of Dada Joe by the Federal Bureau of Investigation (FBI) are untrue, as no official statement from any security agency has been released.

“If indeed Ghana Police, EOCO, and the FBI have apprehended him, what is preventing them from coming out with a statement to say they have arrested him? Once there is no official statement from the FBI, EOCO, and police, then it means there is nothing like that,” he said.

When pressed by Joseph Henry Mensah if the rumors were true, Fred Agyei stated, “I can emphatically say that, because there haven’t been any official statement stating that Joseph Boateng also known as Dada Joe has been picked.”

Fred Agyei further noted that Dada Joe’s team would issue a press statement in the coming days to address the widespread speculations on the matter.

“We are still in the process of coming out with an official press statement to address the issue. When it comes out you would see the content of the statement,” he added.

Background

On May 27, 2025, news broke on social media claiming that Dada Joe had been arrested by the FBI in connection with suspected fraudulent activities.

Over the years, Dada Joe has frequently gone viral on social media for his lavish lifestyle.

He was said to have purchased a filling station for $1 million. In 2018, he shared a video of himself importing a Rolls-Royce, and in 2019, he also acquired a Lamborghini Urus.

In response to the news of his alleged arrest, socialite Showboy, who is also Dada Joe’s cousin, took to social media to post a series of cryptic messages.

JHM/MA

Click here to follow the GhanaWeb Entertainment WhatsApp channel

You can also watch an exclusive interview with Ayisi on the latest edition of Talkertainment below:

Ibrahim Mahama, who is a brother of President John Dramani Mahama, and his company, Engineers & Planners (E&P), have sued Bright Simons over what they describe as defamatory statements made in a recent article.

The article, titled “Ghana Provides a Lesson in How Not to Nationalise a Gold Mine”, was published on Simons’ personal website on Saturday, April 19, 2025.

The article discusses Ghana’s management of the Damang gold mine and includes claims that E&P, described as “a powerful operator owned by the brother of Ghana’s President”, suffered financially following a temporary shutdown of operations by Gold Fields.

Simons, a vice president of IMANI Africa, also raised concerns about E&P’s alleged influence on the Minerals Commission, suggesting potential conflicts of interest and political interference.

Ibrahim Mahama, in his application, sought damages of GH¢10 million, among other reliefs.

Below are the full claims in Ibrahim Mahama and his company:

a. A declaration that the statements made by the Defendant, which have been particularised in paragraphs 14(a) and (b) of the statement of claim, are defamatory of the Plaintiffs;

b. An order directed at the Defendant to publish, on the same platforms that he published the defamatory words, as well as a full page of the Daily Graphic newspaper, on six consecutive occasions over a 3-month period, an unqualified retraction and an apology to the Plaintiffs;

c. An order for a perpetual injunction restraining the Defendant, his agents, assigns, and servants from further publishing any defamatory words against the Plaintiffs;

d. General damages of Ten Million Ghana Cedis (GH¢10,000,000.00) for defamation;

e. Costs, including legal fees; and

f. Any other order(s) as this Honourable Court may deem fit.

Meanwhile, the High Court in Accra has ordered Bright Simons, a vice president of IMANI Africa, to file his defence in the defamation suit filed against him by business mogul Ibrahim Mahama.

Court documents sighted by GhanaWeb showed that the IMANI Africa vice president had been commanded to file his defence within 8 days of service.

The court said that if Bright Simons fails to enter his defence within the stipulated time, it will give its judgment on the matter without hearing from him.

“AN ACTION having been commenced against you by the issue of this Writ by the above-named Plaintiff: IBRAHIM MAHAMA & ENGINEERS & PLANNERS COMPANY LTD.

“YOU ARE HEREBY COMMANDED that within EIGHT DAYS after service of this Writ on you, inclusive of the day of service, you do cause an appearance to be entered for you: BRIGHT SIMONS.

“AND TAKE NOTICE that in default of your so doing, judgment may be given in your absence without further notice to you,” parts of the court document, which was issued by the Acting Chief Justice Paul Baffoe-Bonnie on May 28, 2025, read.

L-R: Thomas-Asante, Benjamin Asare and Jordan Ayew featured in Ghana’s loss against Nigeria

GhanaWeb Feature by Benjamin Sackey

The Black Stars’ performance against Nigeria unveiled the brilliance of some players, while others failed to live up to expectations.

The Super Eagles of Nigeria secured a hard-fought 2-1 victory over the Black Stars in the semi-finals of the Unity Cup at the GTech Community Stadium on Wednesday, May 28, 2025, advancing to the tournament final.

This result marks Ghana’s first defeat to Nigeria since 2006, ending a 19-year unbeaten streak against the Super Eagles.

The Black Stars will now face Trinidad and Tobago in the third-place playoff, while Nigeria advances to meet Jamaica in the final on Saturday, May 31, 2025, at the same venue.

This GhanaWeb Sports feature dissects the positives and negatives from the game regarding some players’ performances.

Jordan Ayew

Black Stars captain Jordan Ayew did not have the best game despite creating some decent chances, but they were not enough to find the back of the net.

The Leicester City attacker missed a clear chance that he could have easily tapped into the goalpost to level the score.

The skipper was found holding the ball for too long at some point without being productive, which delayed the team’s transition during counter-attacks.

Razak Simpson

Nations FC defender Razak Simpson was found wanting on several occasions, as he seemed nervous at the initial stages of the game.

The defender was unable to clear the ball in the box, giving Nigeria’s Cyriel Dessers the space to shoot the ball into the net for the opener.

Simpson, who seemed to have lost concentration, scored an own goal when a free-kick was delivered into the penalty box.

Brandon Thomas-Asante

Coventry City striker Thomas-Asante resuscitated the Black Stars’ attack in the second half, constantly threatening the Super Eagles’ defense.

His continuous push paid off as he scored the consolation goal in the 70th minute after latching onto a cross to score.

With Asante’s brilliant performance, he is expected to be part of the Black Stars squad for the 2026 World Cup qualifiers.

Benjamin Asare

Accra Hearts of Oak goalkeeper Benjamin Asare put up a decent performance despite conceding two goals in the first half of the game.

Although the goals were not primarily his fault, he made some crucial saves to keep Ghana in the game and prevent an embarrassing scoreline.

Caleb Yirenkyi

The FC Nordsjaelland player was deployed at right-back in the second half and adapted seamlessly.

Composed and energetic, Yirenkyi demonstrated strong defensive awareness, making timely interceptions and tracking runs effectively.

His precise passing stood out, contributing to a smoother build-up from the back and helping Ghana dominate stretches of the second half.

Meanwhile, watch as ADISEC win the 4×200 Boys finals at the 23rd Annual Inter schools and colleges

A prominent member of the National Democratic Congress (NDC), Professor Avea Nsoh, has criticized the opposition New Patriotic Party (), whose appointees are currently under investigation by National Security and other crime investigative agencies over alleged offences.

The most recent figure to come under scrutiny is the NPP’s Ashanti Regional Chairman, Bernard Antwi Bosiako, popularly known as Chairman Wontumi, who was picked up by the Economic and Organized Crime Office (EOCO).

President John Dramani Mahama has commenced a three-region “Thank You” tour, beginning Thursday, May 29, in the Bono East Region.

The tour is part of his nationwide appreciation campaign to express his heartfelt gratitude to the people of Ghana for the overwhelming support and confidence they showed in him during the December 2024 general elections.

The President is expected to address a grand durbar of chiefs, opinion leaders, and residents in Bono East, where he will personally thank them for their massive turnout and the resounding endorsement they gave him and the National Democratic Congress (NDC) at the polls.

The durbar will serve as an important platform for President Mahama to reaffirm his commitment to inclusive leadership and participatory governance.

In addition to expressing gratitude, President Mahama will also take the opportunity to outline his administration’s development agenda for the region.

He is expected to unveil a number of priority projects tailored to meet the specific needs of the people, with a focus on job creation, youth empowerment, education, healthcare, and infrastructure development.

Read also…

Health Ministry: Nearly 100,000 trained health workers unemployed

Ghana’s Minister for the Interior, Muntaka Mohammed Mubarak, on Wednesday, May 28, 2025, received the Ambassador of Qatar to Ghana, H.E. Khalid Bin Jabor Al-Mesallam, at his office in Accra.

The courtesy call was aimed at deepening diplomatic relations and exploring new areas of cooperation between the two countries.

In their discussions, Honorable Muntaka expressed appreciation for the Ambassador’s visit and reaffirmed Ghana’s commitment to regional security.

He highlighted the Ministry’s initiatives in securing the nation’s borders and outlined opportunities for Qatari support to the Ghana Prisons Service, particularly in the development of industrial hubs to promote inmate rehabilitation and skills training.

Both officials emphasized the importance of collaborative efforts to advance mutual interests and improve the well-being of their respective citizens.

The meeting ended with a reaffirmation of the shared commitment to strengthening the longstanding ties between Ghana and Qatar.

Ato Forson appointed Returning Officer for AfDB presidential elections

The Governor of the Bank of Ghana, Dr. Johnson Asiama, has urged Ghanaian businesses to prioritise the use of the cedi in their transactions.

According to Dr. Asiama the over-reliance on foreign currencies could undermine recent economic progress.

Speaking at the 9th Ghana CEO Summit in Accra, he said the cedi has shown strong performance in recent weeks, appreciating by nearly 19% between April and May, 2025.

He attributed this to prudent fiscal management and improved market confidence, and not direct dollar interventions by the central bank.

“We are not supporting the currency by using our international reserves. We are supporting the economy through sound monetary policy, and we expect businesses to support this effort by transacting in cedis,” Dr. Asiama said.

He reiterated his call on the business community to support the central bank’s efforts by choosing the cedi as the currency of choice for all local transactions.

“Let me emphasise that the cedi is our sole currency and a legal tender in Ghana so businesses should do business with the cedi,” he said.

The Governor emphasised that while the Bank of Ghana is not targeting an over-appreciation of the cedi, indicating that maintaining stability in the exchange rate is critical to sustaining economic recovery, controlling inflation, and building investor trust.

He noted that increased usage of foreign currencies in local transactions puts pressure on the cedi and hampers national efforts to stabilise the economy.

The Paga Youth Movement (PAYOM) has made a passionate appeal to the government of President John Dramani Mahama to consider upgrading the long-standing Paga/Navrongo Airstrip into a full-fledged regional airport for the Upper East Region, describing the move as the most cost-effective, technically feasible, and economically viable option available.

At a press conference held in Paga, the youth group expressed appreciation for President Mahama’s recent directive to the Ghana Airports Company Limited (GACL) to pursue a Public-Private Partnership (PPP) model in the development of a regional airport in the Upper East Region.

However, PAYOM in a statement sigend by its Public Relations Officer, Desmond Ayambire Abire, noted with concern that current discourse and actions surrounding the project appear to sideline the Paga/Navrongo Airstrip, despite its historical significance and existing infrastructure.

Concerns Over One-Sided Approach

According to PAYOM, recent media commentaries and the actions of key public officials, including the Chief Executive Officer of the GACL and the Upper East Regional Minister, suggest a bias toward a new site at Anateem—some 15km from Bolgatanga and 30km from the Paga border. They decried the lack of a comprehensive assessment of the existing Paga/Navrongo Airstrip, stating that this undermines transparency and fairness in such a significant public investment.

“Radio stations and social media platforms have been dominated by a one-sided campaign, with no indication that officials have even visited the Paga/Navrongo site. This gives the impression that decisions have already been made without stakeholder consultation,” the group stated.

They questioned why proximity to Burkina Faso is being cited as justification for the Anateem site when Paga itself lies directly on the Ghana-Burkina border, making it even more strategic from a regional trade and security standpoint.

Historic Significance and Technical Feasibility

Constructed in 1939 and completed in 1940 by the colonial administration, the Paga/Navrongo Airstrip was originally built for military purposes and has served Ghana for over eight decades. PAYOM cited previous feasibility studies, including one under the late Hon. Joseph Kofi Addah as Aviation Minister, which confirmed the site’s technical and financial viability for conversion into a domestic airport.

“With government now seeking private sector participation, upgrading an existing airstrip offers far greater value to investors than developing a new airport from scratch,” the group argued, stressing that the foundational infrastructure already in place at Paga/Navrongo will reduce capital expenditure significantly.

Strategic and Economic Benefits

PAYOM outlined several compelling reasons why upgrading the Paga/Navrongo Airstrip is the most strategic choice for the region:

Proximity to Burkina Faso and Cross-Border Trade As a key border town, Paga is well-positioned to facilitate trade between Ghana and Sahelian countries like Burkina Faso, Mali, and Niger. A regional airport there would strengthen Ghana’s trade links and consolidate its role as a regional economic hub.

Boost to Tourism and Investment The area is home to major tourist attractions such as the Paga Crocodile Pond and the historic Pikworo Slave Camp, drawing visitors globally. An airport would enhance accessibility, increase tourist arrivals, and attract diaspora investment.

Enhanced Security and Emergency Response In light of ongoing insecurity in the Sahel, PAYOM argued that an upgraded airstrip at Paga would enable faster deployment of security forces and improve national emergency preparedness.

Academic and Cultural Integration

A regional airport in Paga would also encourage educational and cultural exchanges between Ghana and its Francophone neighbours, deepening regional integration.

Traditional and Community Support

PAYOM noted that in June 2020, ten paramount chiefs from the Kassena-Nankana area presented a petition to then-President Nana Akufo-Addo calling for the airstrip’s upgrade. The movement described it as a snub that recent discussions have failed to acknowledge the traditional leaders’ advocacy.

Call to Action

PAYOM is urging the GACL to conduct a comparative assessment of the Paga/Navrongo Airstrip alongside the proposed Anateem site. The group pledged its full cooperation to facilitate a site visit, stating that only an objective evaluation can guarantee that the final decision is technically sound and economically prudent.

They also appealed to private investors to consider the substantial cost-saving potential of upgrading an existing facility rather than building a new one. “We urge the government under President Mahama to give the Paga/Navrongo Airstrip the attention it deserves. It is not just a historical site, but a strategic national asset. Let us invest where it makes the most sense,” the group said.

A Call for Fairness and Transparency

PAYOM concluded by reiterating that their advocacy is not based on parochial interests, but on a desire for fair, data-driven, and inclusive decision-making. “We have kept quiet for far too long, believing that fairness would prevail. But the latest actions suggest a ‘win-loss’ approach rather than mutual benefit. Ghanaians deserve clarity and justification for public investment choices,” they stated.

The Paga Youth Movement, together with the Kassena-Nankana community, affirmed their commitment to supporting government, traditional authorities, private investors, and the media in making the vision of an airport in the Upper East Region a reality—one that maximises impact by building on existing assets.

DISCLAIMER: The Views, Comments, Opinions, Contributions and Statements made by Readers and Contributors on this platform do not necessarily represent the views or policy of Multimedia Group Limited.

DISCLAIMER: The Views, Comments, Opinions, Contributions and Statements made by Readers and Contributors on this platform do not necessarily represent the views or policy of Multimedia Group Limited.

The Acting CEO of the National Petroleum Authority (NPA), Godwin Edudzi Tameklo

The Acting CEO of the National Petroleum Authority (NPA), Godwin Edudzi Tameklo, has disputed the claim that petitioners involved in the ongoing proceedings concerning the removal of Chief Justice Gertrude Torkornoo must personally testify in their case.

Speaking on JoyNews PM Express on May 28, 2025, Tameklo clarified that under Ghana’s jurisprudence, a petitioner is not legally required to testify personally to support their petition.

He explained that the law allows petitioners to call other witnesses to support their claims.

“It is incorrect to suggest that a party must testify on their own behalf in order to prosecute a petition. The law permits petitioners to rely on other witnesses. This is a well-established legal principle and cannot be overlooked,” he said.

He also emphasised that the judiciary cannot compel a petitioner or plaintiff to testify simply because they initiated the process.

“That has never been the position of the law. Petitioners are protected under the law and have the right to choose how they present their case,” Tameklo asserted.

His comments come amid ongoing public debates surrounding the procedure for the potential removal of the Chief Justice, a process governed by Article 146 of Ghana’s 1992 Constitution.

MRA/MA

‘Not surprising’ – Godfred Dame reacts to Supreme Court 5:0 ruling on CJ Torkornoo’s suit

Ghanaian socialite cum music investor, Ayisha Modi

Ghanaian socialite cum music investor, Ayisha Modi, has showered praises on media personality Kofi Adomah Nwanwanii for showing concern during her recent emotional struggles.

In a Facebook post shared on May 28, 2025, Ayisha Modi noted that although Kofi Adomah has not fully recovered from surgery following the gunshot incident, he still took the time to reach out and express concern for her wellbeing.

“Even on your sick bed, you are sooo worried about me. Ahoooooo Kofi Adomah Nwanwanii. What have I done to deserve this kind of love?” she wrote.

Ayisha Modi also extended her gratitude to Kofi Adomah’s wife, Miracle Adomah, for her immense support during this difficult period.

“My brother and my lion king wife, Heaven bless your throne. Just be a good person. Love who you can, help where you can, and give what you can. I appreciate and love you both. Miracle Adomah,” she added.

This post comes shortly after Ayisha Modi shared a troubling Facebook update, detailing the emotional trauma she is battling following the sudden death of her close relative, Nii Adotey.

Read the post below:

JHM/EB

Meanwhile, Ghanaian fashion designer Jude Dontoh shares inspiration behind Lauryn Hill’s Met Gala outfit:

Minority Chief Whip Frank Annoh-Dompreh has proposed a new approach to the local government structure, specifically regarding the election of Municipal, Metropolitan, and District Chief Executives (MMDCEs).

Addressing the floor of Parliament on Thursday, May 29, 2025, the lawmaker stated that the current approach, where the power to appoint MMDCEs rests solely with the highest authority, in this case the President, who nominates individuals subject to approval by assembly members, is not effective.

According to him, the Constitutional Review Committee should include, among the provisions of the 1992 Constitution that require amendment, changes to the process for nominating MMDCEs, recommending that they be elected by the populace, just as is done with the executive and the legislature.

Annoh-Dompreh, who is also the Member of Parliament for Nsawam-Adoagyiri, asserted that the current method often leads to security concerns and violence, as many of the nominees are ultimately rejected by the local population, a worrying trend that has recently been observed in some district assemblies.

“The confirmation of MMDCEs even though largely have been smooth, there have been a number of violent prone areas and incidents all over the country. Just a simple exercise of going to votes on MMDCEs degenerates and it creates security concerns and that must be dealt with. I think one of the process that can be used is the election of MMDCEs,” he said.

Annoh-Dompreh further indicated that the general election of MMDCEs, as opposed to their nomination by the higher appointing authority, the President, would help reduce the unnecessary tensions that often arise.

He also added that the reported cases of violence, which often occur during the confirmation of MMDCEs by assembly members, would be eliminated if the nomination process were amended in the Constitution to allow for a general election by the people to reflect the true will of the electorate and their preferred choice for local leadership.

“It will also reduce the needless tension between MMDCEs and MPs. Our roles are defined significantly different as we play our roles as a legislative arm of government. They have their roles to play. We are almost at each other’s throats needlessly. There are genuine fears where people make the fears that, ‘if we do it [election], the minority will be controlling certain portions of the country and the country will be divided’.”

He added, “It is neither here nor there because that will reflect the will of the people. If it is the will of the people that certain persons should occupy the MMDCE position, you can’t change it. Why is it that the MPs are elected? We are ex official members of the Assembly. The MPs are elected likewise the assembly members who go to confirm the nominees are also elected.”

MAG/MA

Also, watch the latest news in Twi on GhanaWeb TV below:

The Government of Ghana through the Ministry of Finance has announced continued progress in its ongoing debt restructuring negotiations with international creditors, reaffirming its commitment to equitable treatment for all parties involved.

In a statement released by the ministry on May 29, 2025, government assured the public and international stakeholders that discussions with all remaining creditors within the debt restructuring perimeter are advancing constructively.

“In line with Ghana’s commitments to official creditors under the G20 Common Framework, no creditor has been treated preferentially,” the statement read.

“This is consistent with the principle of Comparability of Treatment,” the statement added.

The Ministry also emphasised that Ghana has strictly adhered to the terms outlined in the Memorandum of Understanding signed with official creditors.

This includes maintaining arrears with all external creditors subject to restructuring, a measure aimed at ensuring consistency and fairness across negotiations.

The update signals Ghana’s continued efforts to stabilise its economy and restore debt sustainability through transparent and inclusive restructuring talks.

“The Government remains committed to achieving a fair and mutually beneficial resolution with all creditors and thanks its partners for their forbearance, cooperation, and support,” the statement concluded.

This development follows Ghana’s participation in the G20 Common Framework for Debt Treatment, a global initiative aimed at assisting countries facing unsustainable debt levels through coordinated debt relief and restructuring mechanisms.

Al Nassr are facing growing uncertainty over Cristiano Ronaldo’s future after the Portuguese star posted a cryptic message on social media that appeared to hint at the end of his time at the club.

The forward scored in what is rumoured to have been his final match for Al Nassr, on Monday, May 26, 2025.

A 3-2 defeat to Al Fateh, and followed it up with a statement that has sparked fresh speculation about a possible exit.

Ronaldo, 39, posted:

“This chapter is over. The story? Still being written. Grateful to all.”

The post was accompanied by a picture of him wearing Al Nassr colours, but with no mention of the club or any future plans.

His contract is set to expire this summer, and with no renewal announced, uncertainty over his next move has intensified.

In response, Al Nassr director Fernando Hierro has addressed the situation publicly, admitting that the club is yet to secure Ronaldo’s commitment beyond the current season.

“We are in contact to renew Cristiano’s contract, and we really hope he continues with us here at Al Nassr. His presence from the beginning is a national project. CR7 is a huge phenomenon in the history of football, he helped the Saudi League grow,” Hierro said.

The situation comes at a difficult time for the club, which failed to qualify for the AFC Champions League after Monday’s loss.

Despite Ronaldo giving his side the lead with a 42nd-minute goal, reportedly his 800th in club football, Al Nassr conceded twice late on, ending their hopes of continental football next season.

With the domestic season concluded and Ronaldo’s social media message fuelling exit rumours, Hierro also acknowledged the scale of external interest in the five-time Ballon d’Or winner.

“Every day, a new club appears in the media, with 30 clubs interested in Ronaldo, but we hope he stays,” he added.

Ronaldo joined Al Nassr in December 2022 as part of Saudi Arabia’s major push to attract global football stars.

His arrival opened the door for a wave of high-profile signings in the Saudi Pro League.

But now, with no extension confirmed and growing speculation of a short-term move, possibly for the expanded FIFA Club World Cup, Al Nassr are at risk of losing the face of their sporting transformation.

FKA/MA

Meanwhile, here is why Chairman Wontumi has been served with Exim Bank suit

Olorato Mongale’s murder has sparked public outrage and calls for justice

Police in South Africa have named three men believed to be directly involved in the murder of a university student who had gone on a date.

Olorato Mongale’s body was discovered on Sunday in Lombardy, north of Johannesburg, about two hours after she was reported missing.

Police late on Wednesday said they had seized a VW Polo that was allegedly used in the murder of the 30-year-old student.

“The vehicle was found with traces of blood inside at a panel beater workshop in Phoenix, Durban,” police spokesperson Brig Athlenda Mathe said.

The police also said they had seized the vehicle, a VW Polo, that was allegedly used in the murder of the 30-year-old student.

“The vehicle was found with traces of blood inside at a panel beater workshop in Phoenix, Durban,” said Brig Mathe.

One man, who police believed was the owner of the vehicle, has been arrested.

Photographs of three other suspects – Fezile Ngubane, Philangenkosi Sibongokuhle Makhanya and Bongani Mthimkhulu – who are said to be on the run, have been released by police.

Two of the suspects – Mr Makhanya and Mr Mthimkhulu – were last month arrested for kidnapping and robbing a woman in KwaZulu-Natal, using the same vehicle, police said.

The two are currently out on bail, according to Brig Mathe.

She said the three suspects were “dangerous” and cautioned members of the public not to approach them.

“These suspects are warned to hand themselves over at their nearest police station.”

Ms Mongale was last seen on Sunday in the company of a man she had met a few days earlier at a shopping centre.

CCTV footage showed her leaving a location in Kew, Johannesburg, and walking towards a white VW Polo, with fake licence plates.

Her friends said she was invited for a date by a man only identified as John, who she had met in Johannesburg, where she was studying for a postgraduate degree at Witwatersrand University.

She texted one of her friends shortly before leaving home, saying that she was excited and getting ready for her date.

But police later found her body in an open field, sparking public outrage and calls for justice.

Family spokesperson Criselda Kananda said Ms Mongale’s body was “brutally violated”.

A candlelight vigil was held on Wednesday evening in Lombardi West, at the site where her body was found.

Family and friends have described her as an outspoken, bubbly woman who “lived with purpose and love”, local media reported.

Ms Mongale was a journalism graduate from Rhodes University and worked briefly as a multimedia reporter at the TimesLIVE news website.

While working as a journalist, she covered the murder of Karabo Mokoena – a young woman who was murdered by her boyfriend in 2017.

Ms Mongale’s killing has sparked a fierce debate about the levels of violence faced by women in South Africa.

It is the latest femicide in a country which has a particular problem with violence against women.

About 137 women have been killed and more than 1,000 raped in South Africa between January and March, according to the latest crime statistics.

In 2020, an average of one woman died at the hands of her intimate partner every eight hours, according to a study by the University of the Free State.

In 2019, South Africa ranked among the five countries with the highest rates of the murder of women, according to the United Nations.

The country also has one of the highest rates of sexual violence in the world, with rape being the most reported crime against children.

Communications Director for the New Patriotic Party (NPP), Richard Ahiagbah, believes that the arrest of Chairman Wontumi and other political persecutions being undertaken by the current government is geared towards diverting attention.

According to him, the president, while in opposition, assured the people of Ghana of some bread-and-butter issues that have not seen the light of day.

FIVE PEOPLE are seriously injured and 7 cars have been extensively damaged after a MAN Diesel articulator truck dangerously sped through several vehicles at Alonga Junction in Kumasi on Monday, May 26, 2025 at 2:30pm.

The injured persons, which included pedestrians and occupants of the mangled vehicles, have been identified as Rose Arhin, 48, Martha Owusu, 32, Stephen Osei Tutu, 45, Francis Sakyi Gyan, 38, and Stephen Amponsah, 35.

According to the Manhyia Divisional Police Command statement, which confirmed the accident, all the injured people have since been hospitalized at the Komfo Anokye Teaching Hospital (KATH) in Kumasi.

Narrating how the accident happened, the police report said the articulator truck, registered AS 1129-T, loaded with 1,000 bags of maize, and driven by one Biiyuuk Konlan Godwin, 35, was from Tema and heading to Tanoso in Kumasi.

“On reaching a section of the road at Oforikrom, and was in the process of descending towards Anloga junction, suddenly, suspect driver veered off the road.