{kind=link}

In a country where nearly a quarter of all loans go unpaid, Ghana’s credit market faces serious challenges. But one local fintech solution is quietly rewriting the script.

According to the latest myCreditScore Defaulter Pattern Analysis Report, loans backed by data from myCreditScore show significantly lower default rates than the national average of 23% non-performing loans (NPL).

Thanks to the predictive, data-driven scoring models, lenders using myCreditScore’s platform are making safer, smarter decisions – unlocking financial access for thousands while reducing risk.

Let’s explore why this matters and what the data reveals.

The National Problem: Default Rates at 23%

The Bank of Ghana reports a non-performing loan rate of approximately 23% – meaning nearly one in four loans go unpaid. These defaults cost banks billions of cedis annually, increase interest rates, and limit credit access for responsible borrowers.

The Smart Solution: Predictive Credit Scoring That Works myCreditScore analysed a sample of over 21,000 credit records, including 2,061 confirmed defaulters, to detect behavioural patterns and demographic risk factors. The findings weren’t just insightful – they were game-changing.

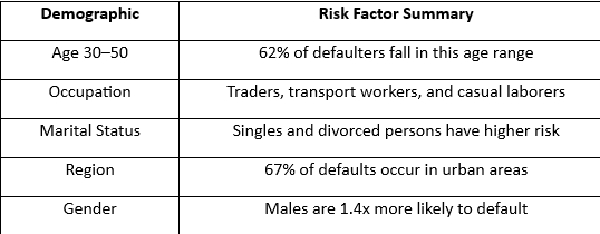

Who Are the Typical Defaulters?

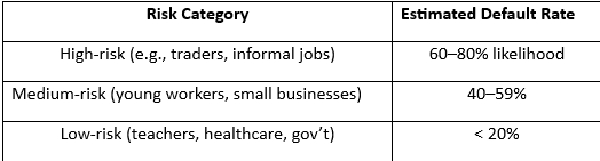

National Default Rate vs. myCreditScore-Backed Loans

Loans filtered through myCreditScore’s predictive engine see up to 65% lower default rates compared to the national average.

Why People Default: The Traps

The data shows that defaulting isn’t random – it follows patterns:

1. Micro-loan traps: 73% of defaulters had loans under GHS 25,000

2. Income instability: 68% worked informally or seasonally

3. Over-leveraging: Average defaulter had 3+ loans and 45%+ debt-to-income ratio

4. Short credit histories: 67% defaulted within 6 months of opening an account

How Does myCreditScore Work Its Magic?

myCreditScore applies a real-time scoring system that factors in:

1. Age, occupation, location, marital status

2. Social media footprint and payment behaviour

3. Tiered risk categorisation and credit limits

4. Rewards for positive repayment behaviour

Predictive Scoring Benefits:

Real Impact: Safer Lending, More Inclusion

According to projections in the report, myCreditScore-backed lenders can expect:

• 25–30% reduction in defaults in 6 months

• 40% faster loan decisions

• 50% lower operational costs for small loans

• A growing customer base built on trust

A Path Forward: Smarter Lending for Ghana’s Future

Ghana’s economic growth depends on accessible, reliable credit, especially for small traders, informal workers, and young entrepreneurs. myCreditScore is proving that with the right data, default is not destiny.

Lenders, banks, and savings & loans companies looking to reduce risk while expanding credit access should take therefore take note. The future of lending in Ghana is data-driven – and the results are already speaking for themselves. If you’re a lender or financial institution in Ghana, consider integrating myCreditScore into your credit assessment workflow.

No developed economy operates without credit and loans. With more than 95% of transactions in Ghana processed as debit transactions, it is very clear that smarter decisions today will build stronger credit systems for our growing economy.